Activity on the Norwegian Continental Shelf

Giants and small fields

The Norwegian Continental Shelf is entering a period of exceptionally high activity in terms of new developments.

By Ulf Rosenberg

Energy, Policy and Public Affairs Advisor

Activity on the Norwegian Continental Shelf

Giants and small fields

The Norwegian Continental Shelf is entering a period of exceptionally high activity in terms of new developments.

By Ulf Rosenberg

Energy, Policy and Public Affairs Advisor

At the same time, the major operators on the shelf are maturing 50-60 new field developments. Almost all of these new projects, however, are small satellite developments – subsea tie-backs.

Exploration activity is also expected to remain high, with around 40 exploration wells planned, although most of these are in well-known areas, with few in new or unexplored waters.

In any case, the Norwegian Continental Shelf will continue to offer attractive business opportunities for both Norwegian and international oil companies, and particularly for the supplier industry. Investments on the shelf in 2025 are estimated at NOK 272 billion – roughly 23 per cent of all real investments in Norway.

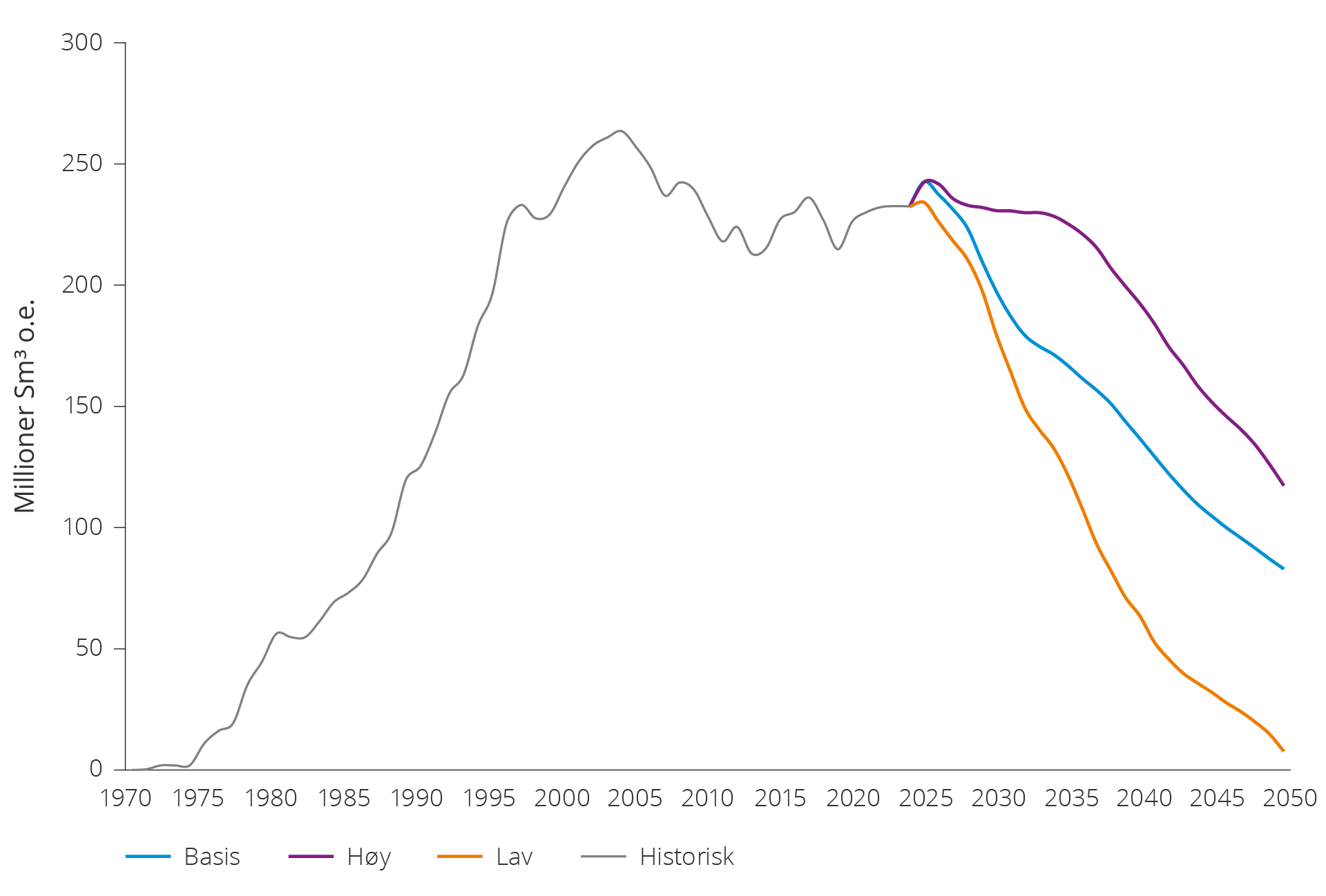

Everything now revolves around realising the top curve in the Norwegian Offshore Directorate’s projection for future production on the shelf. Increased recovery from existing fields and a high number of new discoveries developed into producing assets are the key ingredients in achieving the high scenario outlined in the Directorate’s latest resource report.

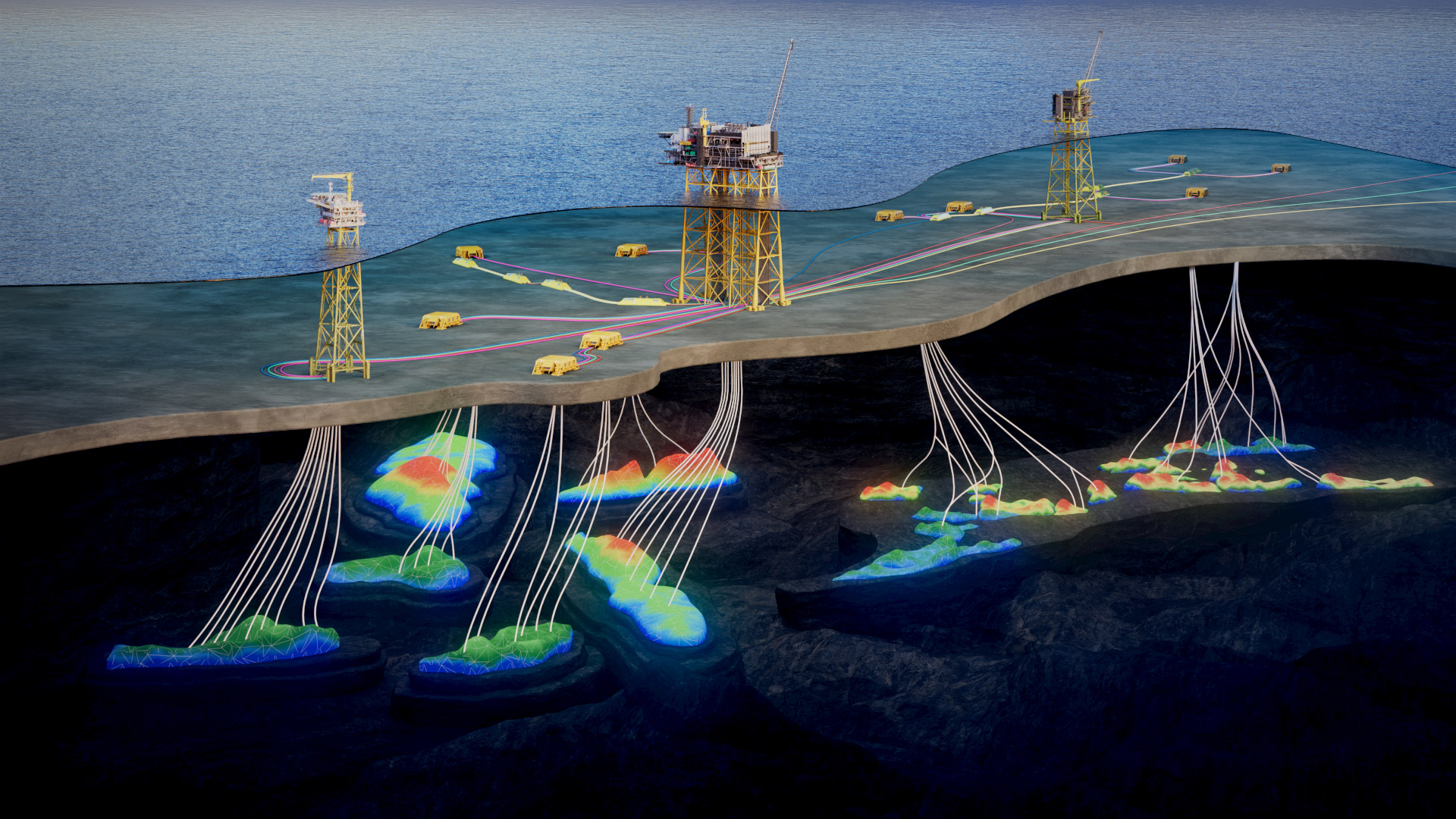

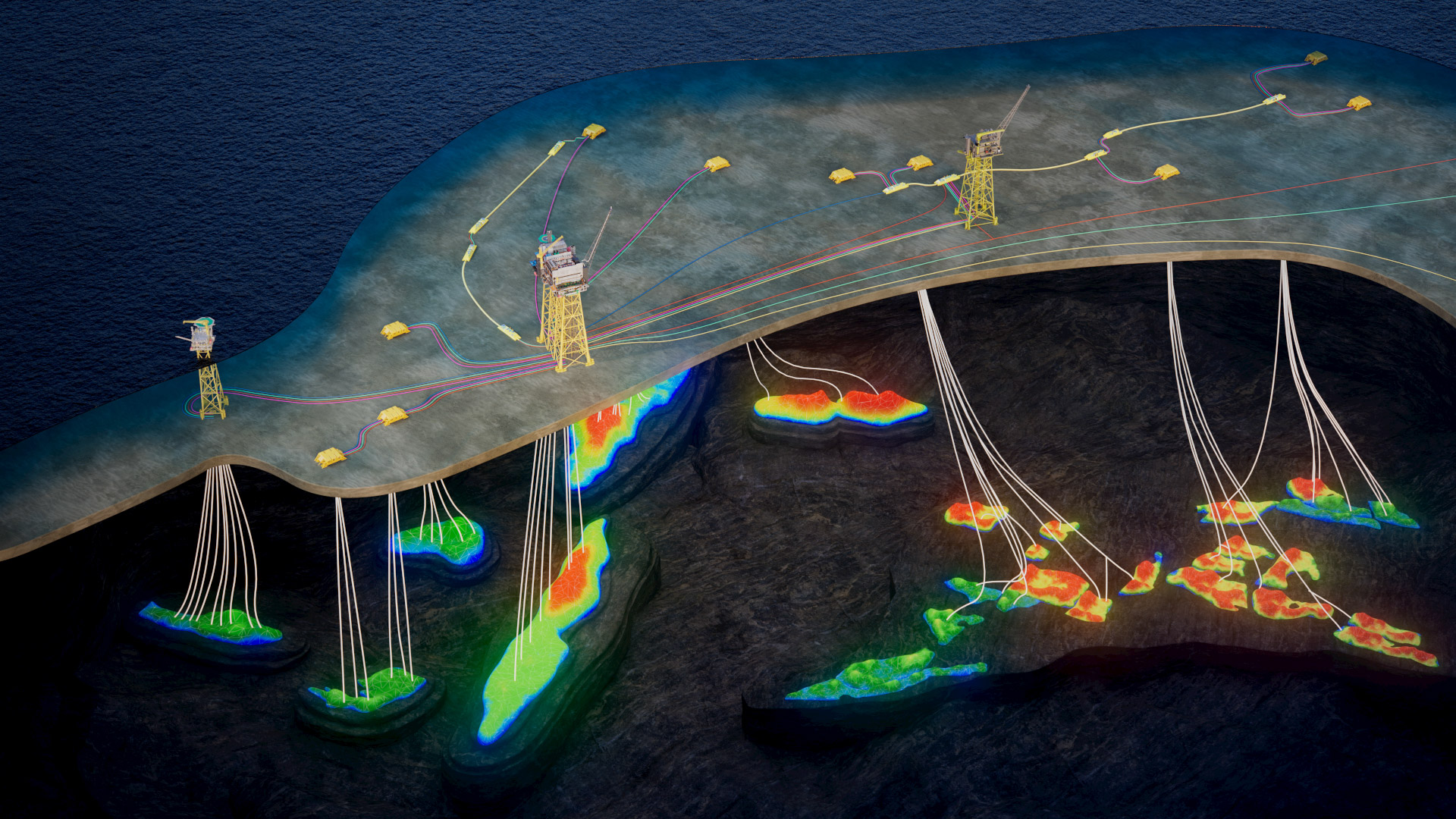

The current high level of activity includes giant projects such as Yggdrasil on one side, and much smaller tie-ins to existing infrastructure on the other. Around the Johan Castberg field – recently brought onstream in the Barents Sea – new discoveries have already been made that can be developed and tied back to the main production vessel.

Around Yggdrasil, discoveries have been made that are already being incorporated into the ongoing development so the new resources can be realised. With its three platforms, Yggdrasil is likely the largest industrial project in Northern Europe today.

Another major ongoing development is in the Valhall area, which has already seen 50 years of activity. With the latest investments, operations there could continue for another 50 years before eventual decommissioning. At the other end of the scale, a number of small discoveries have become commercially viable when combined into a single development, such as the Fram South project. In the Troll area, companies have seen remarkable exploration success in recent years.

There was a rush of new projects after the government adjusted the petroleum tax regime during the pandemic, giving companies incentives to sanction new developments at a time when there were fears of mass unemployment and a drought of orders for the supplier industry – on top of the pandemic’s many other challenges.

“The scheme has produced very good results,” said Prime Minister Jonas Gahr Støre during a offshore yard visit this spring, pointing to the high activity level and significant investment in new technology. The result has been a boom along the coast, with tens of thousands of jobs directly linked to these developments. Altogether, projects worth around NOK 300 billion were sanctioned as a result of the temporary measures.

Some of these projects are already in production, such as Maria Phase 2, Halten East and Ormen Lange Phase 3 in the Norwegian Sea.

Ongoing projects from north to south

Snøhvit Future – Includes onshore compression and electrification of Hammerfest LNG at Melkøya island in Hammerfest Compression will help maintain plateau production and reservoir pressure, while electrification will eliminate major greenhouse gas emissions from the gas turbines that currently power the plant. Operator Equinor has estimated investments at NOK 13.2 billion.

Irpa – A 80 km tie-back to the Aasta Hansteen platform. Gas volumes correspond to the consumption of about 2.3 million UK households over seven years. The project will utilise spare capacity and extend the platform’s life from 2032 to 2039. As Norway’s deepest development at 1,350 metres, it may pave the way for future deepwater projects. OMV is a co-owner of the Aasta Hansteen platform and has made interesting nearby discoveries that may be connected to the installation in the future. Operator: Equinor.

Verdande – A “smaller” NOK 4.7 billion subsea development linking the Cape Vulture and Alve Northeast discoveries to the Norne FPSO. Even such a modest project will create about 1,300 person-years of employment during the 2023–2025 construction phase. The project extends the lifespan and improves the profitability of the Norne field, which has been producing since 1997. Operator: Equinor.

Skarv Satellite Project (SSP) – Three coordinated developments comprising the Alve North, Idun North and Ørn gas and condensate finds. Each will have a subsea installation tied back to the Skarv FPSO off Helgeland. Investments: NOK 16 billion. Around Skarv, there has been notable exploration success, with a number of fields and discoveries named after birds. Operator: Aker BP.

Dvalin North – Norway’s largest discovery in 2021, now being developed as a subsea field tied to the Heidrun platform via Dvalin. Three production wells will be drilled from a subsea template 10 km north of Dvalin. Gas will be exported through the Polarled pipeline to the Nyhamna processing plant. Expected onstream: end of 2026. Operator: Harbour Energy.

Berling – Two separate reservoirs tied back to Åsgard B for processing. Recoverable reserves are estimated at 45 million barrels of oil equivalent, mostly gas. Investments: NOK 9.1 billion. Expected start-up: 2028. Operator: OMV.

Fram South – Combined development of several finds that will export oil and gas via the Troll C platform. Recoverable volumes: 116 million barrels of oil equivalent (75% oil). A number of additional discoveries have also been made in the same area, which are now being matured towards development. Investments: NOK 21 billion. Planned start-up: 2029. Operator: Equinor.

Bestla – Two-well subsea tie-back to Brage, extending the field’s life. Investments: NOK 6.3 billion, with 2,100 person-years of employment. Operator: OKEA.

Yggdrasil – The largest ongoing development on the shelf, and will open up a mature area of the North Sea for new activity. The area consists of the Hugin, Fulla and Munin license groups.

The concept includes a processing platform with a well area and living quarters (Hugin A), which will serve as a central hub for the area. Hugin A is designed for low manning and will operate periodically unmanned after a few years of production. Munin, located in the northern part of the area, will be an unmanned production platform. The Frøy field is being developed with a normally unmanned wellhead platform (Hugin B), which will be tied back to Hugin A.

Yggdrasil also represents an extensive subsea development with a total of nine subsea templates, pipelines and control cables. Fifty-five wells are planned in the area, which will be powered from shore.

The project is expected to contribute around 65,000 person-years of employment in Norway over its lifetime, about half of which will occur during the development phase. There will be activity at yards in Egersund, Stavanger, Haugesund, Stord, Verdal and Sandnessjøen, as well as among several hundred suppliers across the country. In addition, the project will create work and employment for suppliers and fabrication yards worldwide. Operator: Aker BP.

Johan Sverdrup Phase 3 – Johan Sverdrup was the sensational giant on the Norwegian Continental Shelf when it was discovered in 2010. Now, NOK 13 billion will be invested in the third phase of Johan Sverdrup to increase recovery by 40–50 million barrels through new subsea templates and pipelines. The current recovery rate of 66% is world-leading, with an ambition to reach 75%. The average recovery rate on the Norwegian Continental Shelf is 47%. Operator: Equinor.

Eirin – A 1978 gas discovery now extending the life of Gina Krog in the North Sea. The development was fast-tracked in just five months, with first gas planned later this year. Investments: NOK 4 billion. Operator: Equinor.

Symra and Solveig Phase 2 – The development includes a subsea template with four wells tied to the Ivar Aasen installation, with further connection to the Edvard Grieg platform. The NOK 16 billion investment also covers an expansion with additional segments on Solveig, which is linked to the Edvard Grieg field. The operator is Aker BP.

Valhall – Fenris – The Valhall field has already been producing for more than 40 years. The new redevelopment aims to extend production for another 40 years. It includes a new centrally located production and wellhead platform (PWP) with 24 well slots, connected by bridge to the Valhall field centre, and an unmanned installation with eight well slots at Fenris (formerly King Lear), which will be linked to the PWP through subsea equipment and pipelines.

A total of one billion barrels has already been produced from Valhall, and the area is now being prepared for another billion. Investments: NOK 50 billion. Operator: Aker BP.

This overview covers ongoing oil and gas developments. Projects already producing as a result of the pandemic-era stimulus measures, pure electrification projects, and carbon capture and storage (CCS) developments are not included, even though they contribute significantly to environmental performance and asset longevity. Numerous brownfield projects aimed at enhancing recovery are also under way but not listed here.

More than 50 new projects under consideration

Oil companies are currently maturing around 50 discoveries and projects that could help sustain production on the Norwegian shelf over the next decade. Most are tie-backs to existing infrastructure, although one – Wisting in the Barents Sea – could become a new standalone development.

This marks a clear shift from giant platform developments to smaller, cost-effective satellite projects. The list below is not exhaustive but gives an indication of the scale of activity currently under way.

Example new development: Wisting – Located at the northernmost edge of current operations in the Barents Sea. The earlier concept was shelved for cost reasons; a new FPSO-based solution is now being evaluated, with investment decisions expected in 2026.

Example Exploration success: The planned development of Ringvei Vest and the approved Fram South project demonstrate the significant exploration success companies have achieved in the area around Fram and Troll in the waters west of Nordhordland and Sognefjorden. The two Equinor-operated developments cover around ten discoveries made during a highly successful exploration campaign involving several companies. This will strengthen the infrastructure for Fram and Troll, as new discoveries can be phased into existing facilities.

Example old discovery: Garantiana was discovered as early as 2012 by TotalEnergies and later taken over by Equinor. The new operator now plans to drill several exploration wells in the area near Snorre and Visund in the North Sea to strengthen the basis for a potential development. Equinor’s Executive Vice President for the Norwegian Continental Shelf, Kjetil Hove, said last year that Peon could be brought directly to shore, or alternatively tied to Gullfaks or Gjøa. A standalone platform has also been considered previously.

Example rapid expansion: Johan Castberg recently started producing, yet already being explored for additional resources in nearby areas, potentially adding 250–550 million recoverable barrels.

Example: Re-development of closed fields – ConocoPhillips plans to redevelop three fields: Albuskjell,Vest Ekofisk and Tommeliten Gamma, previously shut down as part of Ekofisk II. The fields will be developed using standardised subsea templates — two for Albuskjell and one each for the Vest Ekofisk and Tommeliten Gamma fields. A total of eleven wells are planned. Total investment: NOK 18–20 billion. Recoverable resources are now estimated at between 80 and 120 million barrels. Drilling and subsequent phased production start-up are planned for 2028–2029.

Overview of projects currently under consideration or assessment

North Sea Projects

Albuskjell

Atlantis

Afrodite

Balder Future new phases

Beta

Busta

Carmen

Dugong

EkofiskPPF7

Eldfisk North Extension

Fram Sør

Froskelår

Garantiana

Gjøa subsea-projects

EdvardGrieg/Ivar Aasen basement

Grosbeak

GudrunLPP8

Granegasseksport

JohanSverdrup fase 3

King and Prince

Norma

Ofelia

Othello

Peon

Rhombi

RinghorneNord

RingveiVest

Sigrun/SigrunØst

SleipnerLPP8

Symrafase 2

Tommeliten

Troldhaugen

TrollWest IGR North (TWIN)

ValhallDiatomite

VestEkofisk

ØstFrigg/Epsilon

Norwegian Sea Projects

Adriana/Sabina

Calypso

Erlend/Ragnfrid

Heidrun Extension

Lavrans phase 2

Linnorm

Lunde

Newt

Njord Northern Area

Obelix

Storjo/Kaneljo

Tyrihans nord

Barents Sea Projects

Alta/Gohta

Countach

Goliat gass

Johan Castberg new phases

Lupa

Snøhvit new phases

Wisting